People have always given the advice of saving for the future, but what is the best way to get the most out of your investments?

To most people, saving money means going to the bank and putting it into a savings account. For others, it may be telling the bank to put the money into a GIC or to buy one of their many mutual funds.

GICs makes sense because people are assured by the fact that they know that their principal savings will never be at risk, but they cannot withdraw from the GIC until it is over. Mutual funds are a bit more risky because losses can make investors end up with less than what they started with.

But is this really the best way to save for the future? No, it is not.

This is because of two things banks would rather you do not keep track of. They are inflation and management fees.

Inflation is the general appreciation of goods every year and it is usually around 2%. This means that $100 today will only be worth $98 dollars in a year. This is why McDonalds have always been increasing prices on their menu.

Just by doing NOTHING with your money, you are going to lose 2% a year because of inflation. But if you take that money to the bank and put it into a savings account, it is still almost the same as doing nothing. Normal savings accounts offer abysmally low rates unless you get a special deal from a smaller bank such as Tangerine. Banks like TD Canada trust offer 0.05% on their savings account and 0.50% on their ‘high interest’ savings account. These means you are still losing -1.50% with your money just sitting in the account. Savings accounts are one of the least efficient ways of investing for the future.

GIC

GICs stands for guaranteed investment certificate. Banks offer these for investors that want more gain with the same safety. GICs are guaranteed by the bank, the main drawback being that you cannot withdraw money from your GIC investment until the investing period is over. Which can be a number of years. A 14-month GIC offers 1.75% if you invest less than $10,000. Making you suffer a loss of -0.25% a year!

Mutual Funds

Mutual funds are pushed onto investors by banks and their investment advisors who have to meet sales quotas. For financially slow investors, mutual funds may seem like the best way to invest. You can give your money to a licensed professional who will manage your money for you. The risk level of the mutual fund is predetermined and listed out by the funds, and chosen by the investor. Mutual funds let investors enter their money into a huge pool that then buys up many different types of investments. This lets investors reduce their overall risk level and giving them an opportunity to invest in more expensive securities.

So why are mutual funds a bad investment?

Because of management fees. Mutual funds charge a management expense ratio (MER) onto any profits they generate, the average being around 0.57% according to Morningstar. This means that if your technology mutual fund makes 12% this year, you will only end up with 11.43% as the bank shaves off a portion.

Why pay for such an expensive MER when there is another alternative that offers similar safety and diversity?

ETFs or exchange-traded funds

ETFs or exchange-traded funds are funds that represent a specific industry and/or a level of risk tolerance. If you like technology stocks, why not buy the entire technology industry with QQQ. If you want to buy the entire stock market, you can buy the SPY or the S&P 500. Buying the S&P 500 ETF is the same as owning those 500 companies.

Investors can choose their risk/reward level and their own field of interest, just like a mutual fund. The kicker being that ETFs average only 0.23% (2016) management fees! This means buying a technology ETF earing 12% will leave you with 11.77%.

But you think to yourself, mutual funds are actively managed by licensed professions while ETFs are made to reflect a specific industry (Less active). Shouldn’t mutual funds consistently outperform specific industries and markets?

The answer is no.

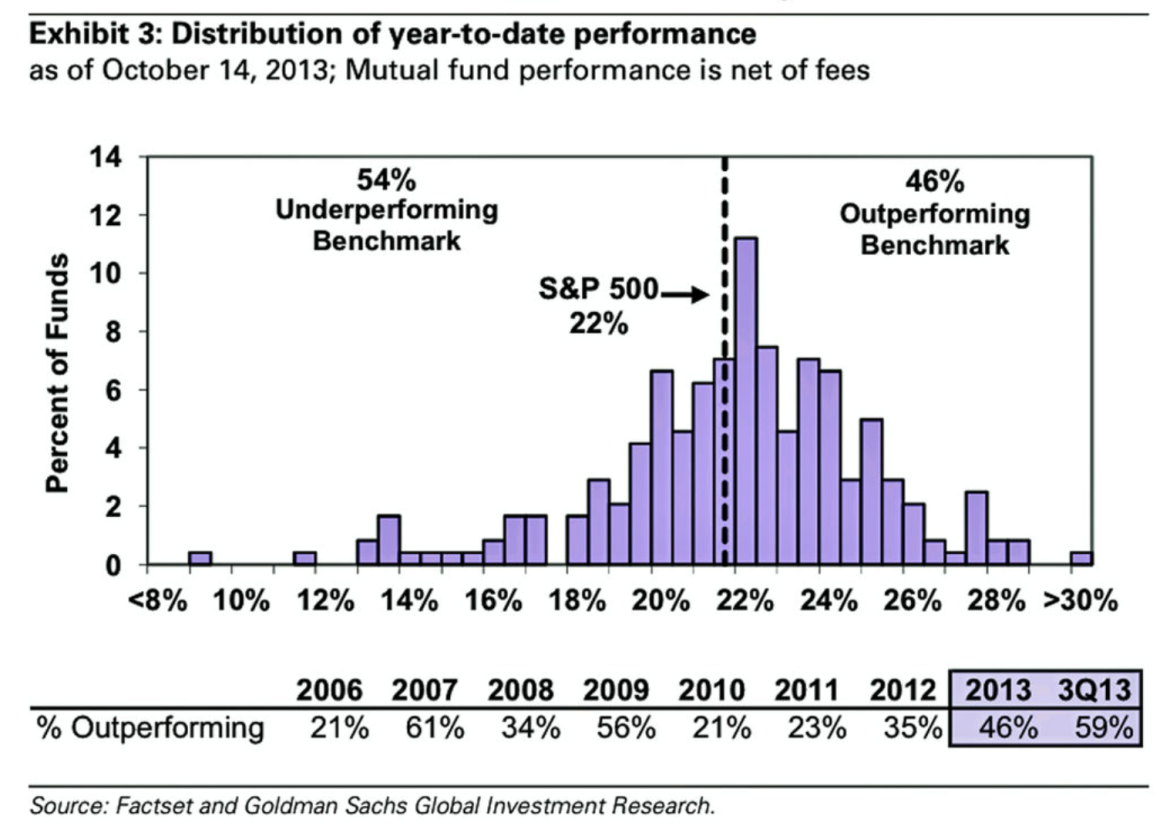

In 2013, after removing the MER from profits, only 46% of mutual funds beat the S&P500! That means more than half of all the mutual funds in the world could not beat the market themselves. All the fancy math and economics that these nicely dressed managers employ are bogus! Why pay extra to have a less than 50% chance of beating the market when you can just buy the market? On top of that, it is not the same 46% that are outperforming the S&P500 every year. There are rarely any funds that can consistently outperform the S&P500.

Let me repeat myself – there are rarely any funds that can consistently beat the market.

So just buy the market!

In summary:

1. Don’t intend to “save” in a savings accounts for long term, as you will be losing money from inflation which is approximately 2%

2. Put your savings in a GIC if you need the money in the short term.

3. If you are going to buy a mutual fund, we recommend to buy an ETF instead.